Financing Restaurant Equipment: Smart Loans & Leases for Pizzerias

Financing your restaurant equipment is a savvy move that lets you get essential gear, like a new pizza prep table, by making manageable monthly payments instead of dropping a huge chunk of cash upfront. It’s a strategy that frees up your capital for other crucial things, like marketing or stocking up on premium mozzarella.

Bottom line? It’s how you get the equipment you need to grow your pizzeria right now.

Equipping Your Pizzeria Without Emptying Your Pockets

Launching a pizzeria or upgrading your current one is an incredible feeling, but the sticker shock from essential equipment can stop you in your tracks. High-temperature deck ovens and those big, refrigerated pizza prep tables are serious investments that directly affect how well—and how fast—you can churn out quality pies.

Paying for all that gear outright can completely drain your cash reserves, leaving you with zero wiggle room for surprise repairs or a killer marketing opportunity. This is exactly where financing restaurant equipment steps in.

Think of it as a bridge that gets you the top-tier equipment you need today while spreading the cost out over time. It’s less about taking on debt and more about making a smart, calculated investment in your pizzeria's future.

Why Financing Is a Smart Move for Pizzerias

For any pizzeria, new or established, cash flow is everything. Financing is one of the best ways to protect it. Instead of one massive cash outlay, you get predictable monthly payments that you can build right into your operating budget. This approach means you can afford better, more reliable equipment from the moment you open your doors.

Here’s why it’s such a game-changer for a pizza business:

- Preserve Working Capital: Keep your cash on hand for the day-to-day stuff—payroll, high-quality flour, and marketing campaigns that get people ordering.

- Access Better Equipment: You can get the high-performance pizza prep table that will actually streamline your workflow, not just the cheapest one you can afford to buy today.

- Generate Immediate ROI: Your new gear starts making you money from day one, which helps cover its own cost over the life of the loan.

This isn't some niche strategy; it's becoming the standard. The global market for restaurant equipment is expected to shoot up from USD 4.8 billion in 2025 to USD 10.2 billion by 2035. That explosive growth is being driven by restaurants looking to get more efficient, and financing is the tool that makes it possible. You can learn more about these market trends and their implications for restaurateurs.

When you finance, you're not just buying a piece of steel; you're investing in a more efficient, profitable kitchen. It’s a powerful tool for turning your pizzeria's vision into a delicious reality without breaking the bank.

Choosing Between a Loan and a Lease

When it comes to financing restaurant equipment, you’re standing at a fork in the road. One path is a loan, the other is a lease. Making the right choice here is one of the most critical financial decisions you'll make as a pizzeria owner, as each option has a completely different impact on your cash flow and long-term business strategy.

Think of it like this: an equipment loan is like buying a house. You borrow money to purchase an asset—your pizza prep table—and you own it from day one. A lease, on the other hand, is like renting an apartment. You pay to use the equipment for a specific period. One builds equity, the other keeps you flexible.

The Case for an Equipment Loan

Taking out a loan is the traditional path to ownership. You make steady monthly payments for a set term, and when the last payment clears, that shiny stainless steel prep table is yours, free and clear. For a piece of equipment that will be a workhorse in your pizzeria for years, that’s a pretty compelling benefit.

The main advantages of buying with a loan are pretty clear:

- Building Equity: Every single payment you make gets you closer to owning an asset that holds real resale value.

- Tax Benefits: You can often deduct the interest you pay on the loan and depreciate the value of the equipment over time, which can seriously lower your tax bill.

- Total Freedom: It's your property. You can modify it, move it, or sell it whenever you want without asking for permission.

The equipment finance market is absolutely massive and growing fast, which tells you just how many businesses rely on these options. It's estimated to be a USD 1.3 trillion industry in 2024 and is expected to climb to USD 1.44 trillion in 2025. This explosive growth shows that financing, including loans, is a standard, battle-tested strategy for getting the gear you need to grow your pizza shop.

The Flexibility of an Equipment Lease

A lease brings a whole different set of advantages to the table, mostly centered on lower upfront costs and adaptability. For pizzerias trying to keep up with the latest tech or those watching their budget closely, leasing a pizza prep table can be a brilliant move.

Here's why leasing is so attractive to many pizzeria owners:

- Lower Monthly Payments: Lease payments are almost always lower than loan payments. That's because you're only paying for the equipment's depreciation during the lease term, not its entire value.

- Easy Upgrades: When your lease is up, you can simply hand back the old model and upgrade to a newer, more efficient one. No more trying to sell outdated equipment on the second-hand market.

- Maintenance Included: Many leases roll maintenance and repair services right into the agreement, protecting you from surprise repair bills that can wreck your budget.

Leasing is all about protecting your cash and staying nimble. It’s the perfect play for the pizzeria owner who wants the best and latest equipment with predictable monthly costs, all without the long-term commitment of ownership.

Let's break down how this looks in the real world with a common piece of equipment.

Loan vs Lease for a Pizza Prep Table

Here’s a side-by-side look at how a loan and a lease might stack up for a typical pizza prep table, giving you a clearer picture of the financial trade-offs.

| Feature | Equipment Loan | Equipment Lease |

|---|---|---|

| Ownership | You own the equipment from the start. | The leasing company owns it; you're just paying to use it. |

| Upfront Cost | Usually requires a down payment, often 10-20% of the total price. | Typically requires only the first and last month's payment, sometimes with no money down. |

| Monthly Payments | Higher, because you're paying off the entire cost of the asset. | Lower, as you're only covering its depreciation during the lease term. |

| End of Term | Once paid off, the equipment is yours to keep, sell, or trade. | You can return it, upgrade to a new model, or sometimes buy it at its market value. |

| Tax Implications | You can deduct interest payments and depreciate the asset's value. | The entire lease payment is usually deductible as an operating expense. |

| Maintenance | You are responsible for all repairs and upkeep once the warranty expires. | Often included in the lease agreement, giving you predictable service costs. |

| Best For | Pizzerias that want to build long-term assets and have stable cash flow. | Startups, pizzerias with tight cash flow, or those who want the latest tech. |

Ultimately, deciding between a loan and a lease comes down to your pizzeria's specific financial situation and your long-term vision.

As you weigh your options, getting a better handle on the different financing models can provide some valuable perspective. It's worth understanding hire purchase vs. lease rental to see the finer details. For a deeper dive focused specifically on outfitting a kitchen, you might also want to check out our guide on commercial kitchen equipment leasing.

Finding the Right Financing Path for You

Once you've weighed owning versus leasing, the next move is figuring out how you'll pay for it. Think of it like planning a road trip. A loan is like buying the car, and a lease is like renting it. Now you need to pick your route—the scenic highway, the fast-moving toll road, or a direct backroad. Each path has its own speed, tolls, and scenery, but they all get you to the same destination: a killer new pizza prep table in your kitchen.

Getting familiar with these routes is the key to landing the best deal for your pizzeria's specific financial situation. Let's walk through the most common ways to finance restaurant equipment, from the old-school banks to the newer online players.

Traditional Bank Loans

This is the classic route, the main highway of financing. Banks usually offer the best interest rates because they play it safe. They want to see that you've been in business for a while, have a solid credit score, and can hand them a business plan that shows you know what you're doing.

If you're running an established pizzeria with a few years of steady profits under your belt, a traditional bank loan is almost always the cheapest way to finance a big purchase, like a top-of-the-line 93-inch pizza prep table. Just be prepared for the journey—the application process can be slow and requires a mountain of paperwork.

Government-Backed SBA Loans

SBA loans are a fantastic option, especially for small businesses or startups that might not check all the boxes for a traditional bank. The Small Business Administration (SBA) doesn't actually give you the money. Instead, it acts as a co-signer, guaranteeing a big chunk of the loan for the bank or credit union that's lending to you.

This government guarantee makes lenders feel a lot safer, which makes it easier for pizzerias like yours to get a "yes." The application can still take some time, but the great terms and lower down payments make SBA loans an incredibly powerful tool for getting the gear you need to grow your pizzeria.

Online Lenders

If banks are the highway, online lenders are the express lane. These tech-savvy companies are all about speed and simplicity. You can often get a decision in a matter of hours and have the money in your account in just a few days. That kind of speed is a lifesaver when your main pizza prep table dies mid-shift and you need a replacement yesterday.

Of course, there's a trade-off. You'll typically pay a higher interest rate for that convenience. But for a pizzeria owner who needs cash fast or has a credit history that's less than perfect, an online lender is an amazing resource for securing fast and flexible financing restaurant equipment.

"The key is to match the financing vehicle to your business's immediate needs and long-term goals. A fast, flexible loan might be perfect for an emergency replacement, while a long-term SBA loan could be the foundation for a full kitchen expansion."

Vendor or Manufacturer Financing

Sometimes, the simplest path is the best one. A lot of equipment suppliers—including the folks who sell pizza prep tables—offer their own financing right at the point of sale. It's often called vendor financing, and it's incredibly convenient because you handle the purchase and the loan all in one conversation.

Because the vendor's main goal is to sell the equipment, they can sometimes offer killer promotional deals, like 0% interest for the first year. This can be an unbeatable way to get a specific piece of equipment, like a new Atosa or True pizza prep table, straight from a source you trust. You can see how these programs stack up by checking out our detailed guide on restaurant equipment financing.

This isn't just a niche strategy; it's a huge trend. A recent industry report found that over 50% of restaurant owners were planning to spend more on equipment. Even more telling, 67% were specifically looking to replace kitchen gear to make their operations more efficient. You can read the full report on restaurant sector equipment finance trends for a deeper dive.

How to Prepare a Winning Application

Trying to get the best financing terms for your pizza prep table is a lot like perfecting a pizza recipe—it’s all about having the right ingredients and doing the prep work. Lenders want to see a clear, compelling story about your pizzeria's financial health and where it's headed. A sloppy, disorganized application can get you stuck with higher interest rates or even an outright "no," even if your business is making good money.

Your mission is to hand them a package that screams "safe investment." That means getting your documents in order, polishing your financial story, and showing the lender you’ve got a real plan to turn their loan into more revenue from that shiny new pizza prep table. It's all about building their confidence from the very first page.

Assembling Your Essential Documents

Before you even think about filling out an application, you need to get your paperwork sorted. Lenders have a standard checklist of documents they use to verify that your business is real, stable, and profitable. Think of these as the essential toppings for your application—without them, it's just not complete.

You'll almost always need to have these ready:

- Business Plan: A quick, sharp summary of your pizzeria. What's your concept? Who's your target market? And how is this new pizza prep table going to make you more money?

- Financial Statements: This is the big three: your balance sheet, income statement, and cash flow statement. If you've been around for a bit, they'll want to see the last two or three years.

- Bank Statements: Most lenders will ask for three to six months of your most recent business bank statements. They want to see your day-to-day cash flow.

- Business and Personal Tax Returns: Get ready to hand over at least two years of returns. This gives them the complete financial picture.

- Credit Reports: They're going to pull both your personal and business credit scores. Expect them to be looked at very closely.

A strong application is built on clear financial data. To really show them you know your stuff, a great first step is understanding your financial statements.

Strengthening Your Financial Profile

Just having the documents isn't enough. It's what's in those documents that really counts. Your credit score, for instance, is one of the heaviest hitters. A higher score—you really want to be above 680—shows a history of borrowing responsibly and can unlock much better interest rates.

If your score is a little lower than you'd like, take some time to improve it before you apply. Start chipping away at existing debts, check your report for any errors you can dispute, and make absolutely sure every single payment is on time. Even small bumps to your score can make a huge difference in the loan terms you get offered.

For brand-new pizzerias, having a detailed list of every potential expense is absolutely critical. You can get a great head start by checking out our complete guide on restaurant startup costs to make your business plan that much stronger.

Your business plan is more than a formality; it’s your chance to tell a story. Clearly explain why you need that specific pizza prep table. Project exactly how its efficiency will boost your pizzeria's revenue. A well-argued plan can often make up for a shorter time in business or lower annual revenue.

Financing a Pizza Prep Table From Start to Finish

Alright, let's put all this theory into practice. To show you how financing restaurant equipment works in the real world, we'll walk through the process with a pizzeria owner who needs a new, multi-door refrigerated pizza prep table. This isn't just an abstract concept; it's a clear, actionable game plan you can follow.

It all starts with a problem you need to solve. Maybe your old unit is on its last legs and can't hold a consistent temperature. Or perhaps your business is booming, and you desperately need more refrigerated storage and a bigger prep surface just to keep up with the ticket machine.

Step 1: Select the Right Equipment and Get Quotes

First things first, you need to pinpoint the perfect pizza prep table for your kitchen's unique workflow. Are you a small shop that can get by with a compact 44-inch model, or do you need a beastly 93-inch workstation to handle the Friday night rush? Think about the features that matter to you—how many doors, pan capacity, and whether you want drawers for easier access to dough balls.

Once you have a model in mind, don't just take the first offer you get. Shop around. Reach out to at least three different financing sources. I recommend talking to a traditional bank, an online lender, and even the equipment vendor directly. This is the only way to compare interest rates, term lengths, and fees to find the deal that truly works for your bottom line.

Step 2: Complete and Submit Your Application

With quotes in hand, it's time to pick the best offer and make it official. This is where all that document preparation we talked about earlier really pays off. You’ll be submitting your business plan, financial statements, tax returns, and bank statements, likely through the lender’s online portal.

Make sure every single field is filled out accurately and that all your documents are clear and current. A clean, complete application sends a strong message of professionalism. It can seriously speed up the review process and get you that much closer to an approval.

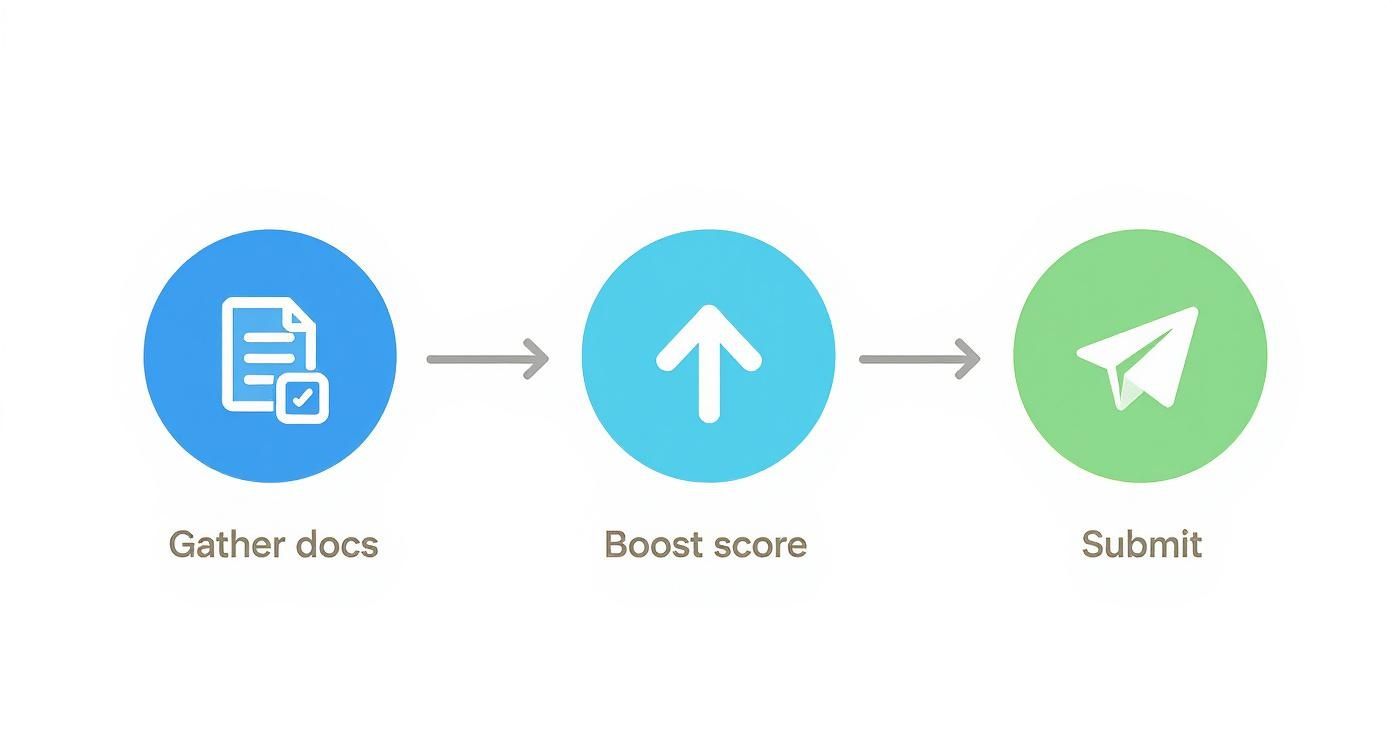

This infographic breaks down the core elements of a successful financing application.

As you can see, a winning application is built on a foundation of solid paperwork and a strong financial story.

Step 3: Review the Offer and Sign the Agreement

After you hit "submit," the lender will get to work reviewing your file. This can take anywhere from a few hours to a couple of weeks, depending on the lender. If you're approved, they'll send over a formal financing offer. Don’t just glance at it—read every single line. This is important.

Pay close attention to these key details:

- The Interest Rate: Is it fixed or variable? This number represents the true cost of borrowing the money.

- The Term Length: How many months are you on the hook for payments? A longer term gives you lower monthly payments, but you'll pay more in interest over the life of the loan.

- Any Fees: Keep an eye out for origination fees, documentation fees, or prepayment penalties that can sneak up on you.

This is your last chance to make sure the terms align with your pizzeria's budget and your long-term goals. If it all checks out, you’ll sign the financing agreement and make it official.

Step 4: Receive Funds and Purchase Your Equipment

This is the exciting part. Once the agreement is signed, the lender will release the funds. Sometimes, they'll pay the equipment supplier directly, which simplifies things. Other times, the money will be deposited straight into your business bank account.

With the funding secured, you can finally place the order for that brand-new pizza prep table. You've successfully navigated the financing maze, landing a crucial, revenue-generating asset for your kitchen—all without draining your cash reserves.

Common Questions About Equipment Financing

Even with a solid plan, a few questions always pop up when it's time to talk about financing restaurant equipment. Getting straight answers is the key to feeling confident that you're making the right call for your pizzeria.

Let's tackle some of the most common questions we hear from pizzeria owners who are looking to finance essential gear like their next pizza prep table. This should help clear up any lingering uncertainties so you can move forward with a full picture of the process.

What Credit Score Do I Need for Equipment Financing

This is the big one, isn't it? It’s what keeps a lot of pizzeria owners up at night. While every lender has their own rules, most traditional banks really like to see a personal credit score of 680 or higher. A score in that range shows you have a solid history of paying your bills, and it's usually your ticket to the best interest rates.

But don't panic if your score isn't quite there. Plenty of online lenders specialize in working with business owners who have a few bumps in their credit history, sometimes accepting scores as low as 550. Just know that a lower score almost always means you’ll face higher interest rates to balance out the lender's risk.

It’s always a smart move to pull your credit report and check for errors before you start applying. Cleaning up even small issues can give your score a little boost, which can lead to big savings over the life of your loan.

Can I Finance Used Pizza Ovens or Prep Tables

Absolutely. In fact, many lenders are happy to finance used pizza equipment, and this can be a fantastic way to save some serious cash. Grabbing a pre-owned pizza prep table can stretch your budget, freeing up money to invest in other critical areas like marketing or that first big inventory order.

The financing terms for used gear might look a little different, though. Lenders often prefer shorter repayment periods for used equipment since it has a shorter expected lifespan. They may also ask for a professional appraisal to confirm the item's age, condition, and fair market value before they cut the check.

How Fast Can I Get Funding for My Equipment

The timeline for getting your hands on the cash really depends on who you borrow from. This is a huge deal if your main pizza prep table just died and you need a replacement, like, yesterday.

- Traditional Banks & SBA Loans: Think slow and steady. Their deep-dive underwriting process can take several weeks, and sometimes a couple of months, from the day you apply to the day the money hits your account.

- Online Lenders & Equipment Financiers: These guys are built for speed. Many can give you an approval in under 24 hours and get the funds into your account in as little as two to three business days.

If you're in an emergency—say, your main prep table gives up the ghost during a Friday night rush—an online lender is almost always your fastest way out of a jam.

Will Financing Cover Delivery and Installation Costs

In many cases, yes! This is a huge perk that can save you from getting hit with unexpected out-of-pocket costs. Many specialized equipment financing companies let you roll these "soft costs" right into your total loan amount.

These costs often include things like:

- Delivery and freight charges

- Professional installation fees

- Initial setup and staff training costs

When you're getting quotes, make it a point to ask each lender if these extra costs can be bundled into the loan or lease. It’s a simple question that can make a massive difference to your cash flow.

At Pizza Prep Table, we know the right equipment is the heart and soul of your pizzeria. We offer flexible lease-to-own financing plans to help you get the high-quality refrigerated prep tables you need without the upfront financial hit. Check out our selection and find the perfect financing solution for your business at https://pizzapreptable.com.